Every GST Filing Period Creates The Same Problem.

Invoices are missing.

Suppliers upload returns late.

GSTR-2A shows one thing.

GSTR-2B shows another.

And accounting teams still spend hours comparing reports manually before finalizing ITC claims.

In many accounting firms, GST reconciliation becomes stressful not because of GST itself, but because invoice matching and ITC validation still depend heavily on manual checking.

This is exactly why understanding GSTR-2A and GSTR-2B properly matters.

Using the right report at the right stage helps reduce reconciliation confusion, ITC mismatches, and unnecessary compliance pressure.

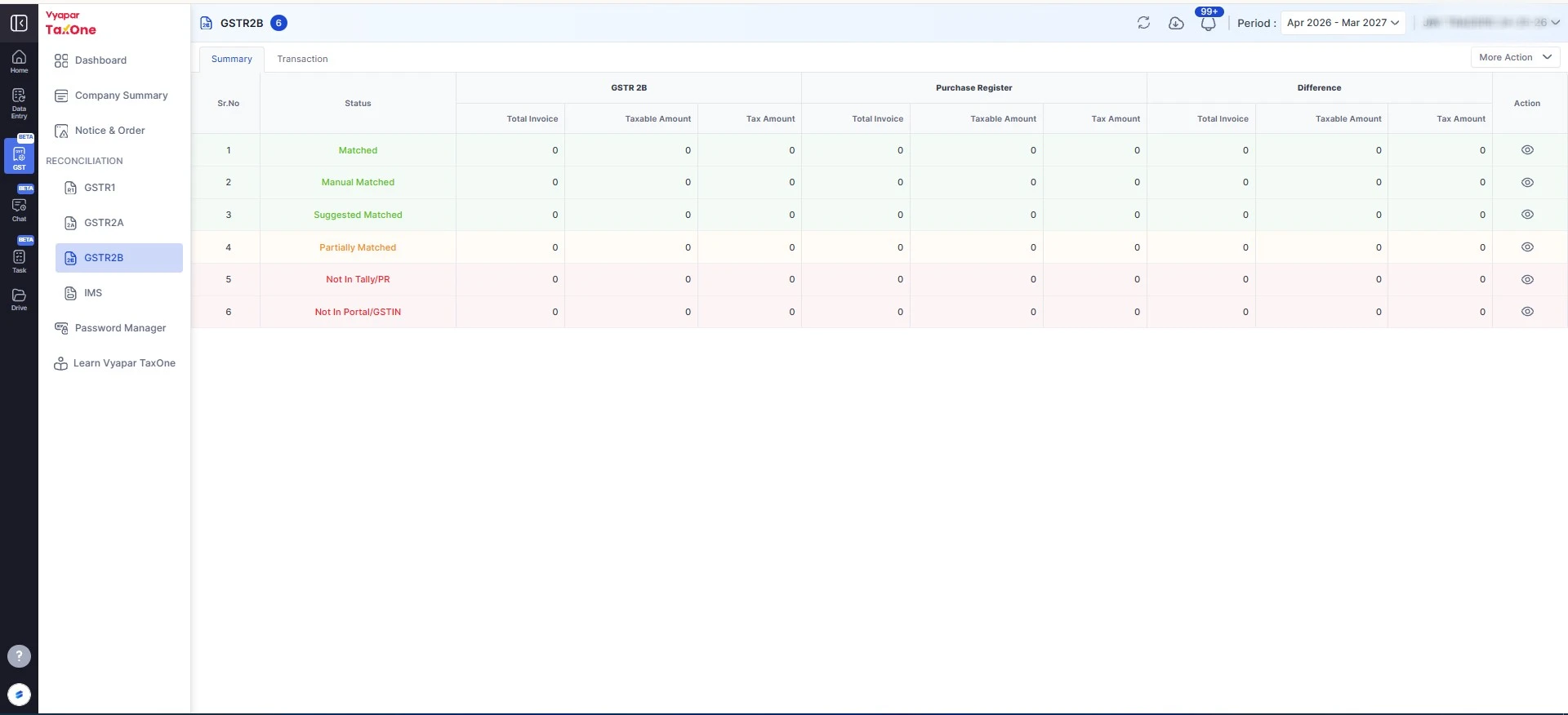

What Is the Difference Between GSTR-2A and GSTR-2B?

GSTR-2A is a dynamic report that keeps updating whenever suppliers upload or modify invoices.

GSTR-2B is a fixed monthly statement used for final ITC claims.

In simple terms:

- GSTR-2A helps track invoice activity

- GSTR-2B helps finalize eligible ITC

Both reports are important, but they serve different purposes in GST reconciliation workflows.

When Should Accounting Teams Use GSTR-2A?

GSTR-2A is mainly useful during ongoing reconciliation activities.

Accounting teams usually use it for:

- tracking supplier invoice uploads

- identifying missing invoices

- checking vendor compliance

- monitoring invoice amendments

Since the report updates continuously, it helps teams catch reconciliation issues before final GST filing.

When Should Accounting Teams Use GSTR-2B?

GSTR-2B is generally used during final GST return filing.

Since the report remains fixed for a tax period, it helps accounting teams:

- validate eligible ITC

- avoid last-minute invoice changes

- finalize GST reconciliation

- reduce ITC claim mismatches

In most workflows, GSTR-2B becomes the final reference point for ITC claims.

GSTR-2A vs GSTR-2B: Key Differences

| Feature | GSTR-2A | GSTR-2B |

|---|---|---|

| Nature | Dynamic | Static |

| Updates | Real-time updates | Fixed monthly statement |

| Main Use | Ongoing reconciliation | Final ITC claim |

| Changes After Generation | Data from supplier filings | Consolidated supplier data |

| Best Used For | Invoice tracking | Invoice tracking |

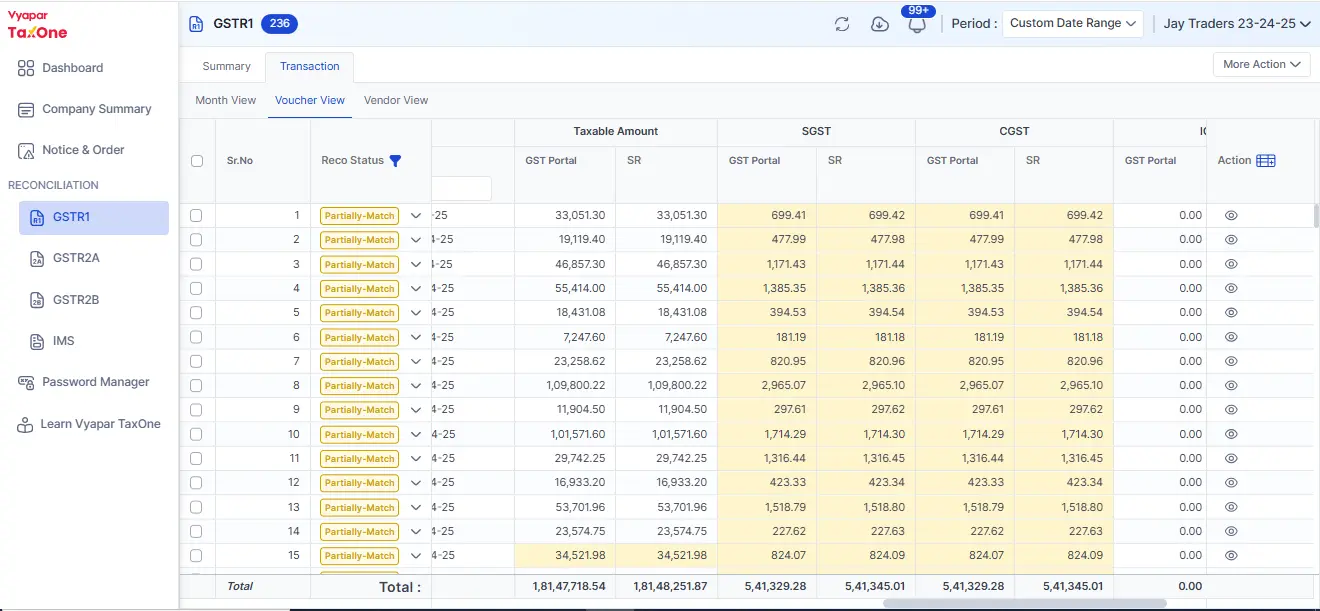

Common GST Reconciliation Problems

In high-volume accounting environments, reconciliation delays usually happen because of:

- supplier filing delays

- missing invoices

- incorrect GST values

- duplicate entries

- Excel-based reconciliation workflows

- manual invoice checking

And during GST filing periods, these small mismatches often create major operational pressure. This is one of the main reasons accounting teams are gradually moving toward automated GST reconciliation workflows.

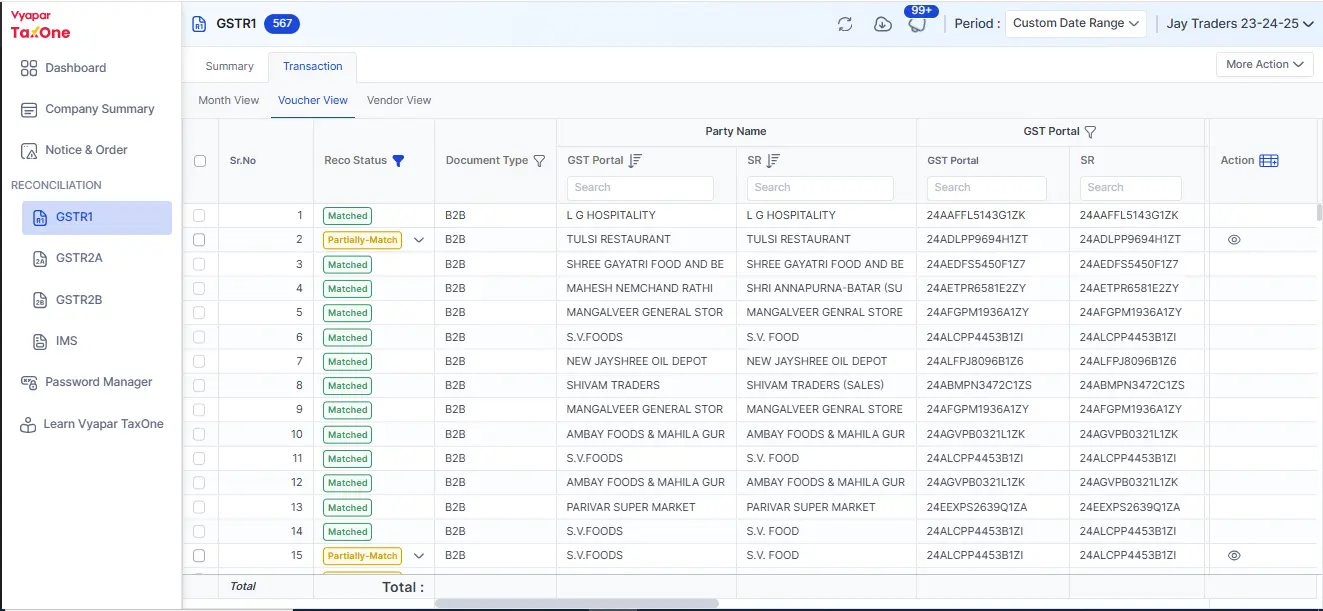

How We Simplify GST Reconciliation Workflows

Manual reconciliation becomes difficult when invoice volumes increase across multiple vendors and GST periods.

We help accounting teams reduce repetitive checking efforts by simplifying:

- invoice matching

- mismatch identification

- ITC validation

- reconciliation tracking

This helps teams process reconciliation faster while improving accuracy during GST filing periods.

You can explore our GST reconciliation workflow here: https://taxone.vyapar.com/gst-reconciliation-feature

For more insights, check out our guide on performing a perfect GSTR 2A reconciliation within Tally in 7 simple steps.

Reduce GST Reconciliation Work Without Increasing Manual Effort

In many accounting teams, GST reconciliation still depends heavily on Excel comparisons, manual invoice checking, and repeated vendor follow-ups.

As transaction volumes increase, these workflows become difficult to manage efficiently during filing periods.

We built our GST reconciliation workflows to help accounting teams reduce repetitive checking efforts, identify mismatches faster, and process ITC validation more accurately across GSTR-2A, GSTR-2B, and purchase data.

With automated reconciliation, invoice matching, and real-time mismatch visibility, teams can spend less time managing spreadsheets and more time focusing on compliance accuracy.

If your team is still spending hours manually validating GST data every month, this is the right time to simplify the workflow.

Experience how Vyapar TaxOne simplifies your workflow by signing up for a free 7-day trial of our GST Reconciliation feature.

Questions Accounting Teams Usually Ask About GSTR-2A & GSTR-2B

Why does GSTR-2A show invoices that are missing in GSTR-2B?

This usually happens when suppliers upload or amend invoices after the cut-off period used for generating GSTR-2B. Since GSTR-2A updates continuously and GSTR-2B remains fixed for a tax period, both reports may temporarily show different invoice data.

Why do accountants prefer GSTR-2B for final ITC claims?

In most GST workflows, accounting teams rely more on GSTR-2B because it provides a fixed monthly view of eligible ITC. This helps reduce last-minute reconciliation changes during GST filing.

Can late supplier filing affect ITC reconciliation?

Yes. Supplier delays are one of the most common reasons for GST reconciliation mismatches. If invoices are uploaded late, they may appear in GSTR-2A but not in the current GSTR-2B period.

Why does GST reconciliation still consume so much time for finance teams?

In many accounting environments, reconciliation still depends heavily on Excel comparisons, manual invoice checking, and vendor follow-ups. As invoice volumes increase, these workflows become difficult to manage manually.

What creates the highest reconciliation workload during GST filing periods?

Most accounting teams spend significant time:

- identifying missing invoices

- validating ITC eligibility

- checking duplicate entries

- comparing purchase records with GST reports

- coordinating with suppliers for corrections

Is GSTR-2A enough for claiming ITC?

No. GSTR-2A is useful for ongoing invoice tracking and reconciliation, but accounting teams generally use GSTR-2B as the final reference for ITC claims because it is static for the tax period.

Why do GST mismatches happen even when invoices exist in books?

Mismatches usually happen because:

- suppliers file returns late

- invoice details are incorrect

- GST values differ

- invoices are amended later

- duplicate entries exist

- invoices are uploaded in different tax periods

How are accounting teams reducing manual GST reconciliation work today?

Many accounting teams are gradually moving toward automated reconciliation workflows that help identify mismatches faster, compare invoices automatically, and simplify ITC validation across GSTR-2A, GSTR-2B, and purchase records.

Why is Excel-based GST reconciliation becoming difficult at scale?

As transaction volumes grow, manual spreadsheet-based reconciliation becomes harder to track accurately. Multiple invoice versions, supplier amendments, and large GST datasets usually increase the chances of human error and reconciliation delays.

What should accounting teams reconcile apart from GSTR-2A and GSTR-2B?

In most workflows, accounting teams also reconcile:

- purchase registers

- GSTR-3B

- supplier invoices

- ITC claims

- vendor compliance data